Japan’s moment: Why the market no longer needs the world to cooperate

Man Japan Core Alpha’s Emily Badger says the domestic story makes Japan one of the most compelling – and overlooked – opportunities in global equity markets right now.

- Matteo Anelli

- 6 min reading time

Source: Trustnet

For most of the past three decades, investing in Japan meant gaining exposure to export-oriented manufacturers, global automakers and technology conglomerates – the case for Japanese equities was the case for global growth. However, this is now changing, said Emily Badger, co-manager of the £2.8bn Man Japan Core Alpha fund.

“Japan has this independent and unique story at the moment,” she said. “It’s quite different to the US-focused story and it’s a story that isn’t vulnerable to the threat of AI.”

The fund has been running the same contrarian value approach since its inception in 2006 and has delivered a 202% return over 10 years, placing it in the top decile of the IA Japan sector over that period. It holds the maximum five FE fundinfo crowns.

Below, Badger argues that the end of deflation, a corporate governance revolution that is finally unlocking value and a labour market that is defying its demographic headwinds, aren’t just a blip.

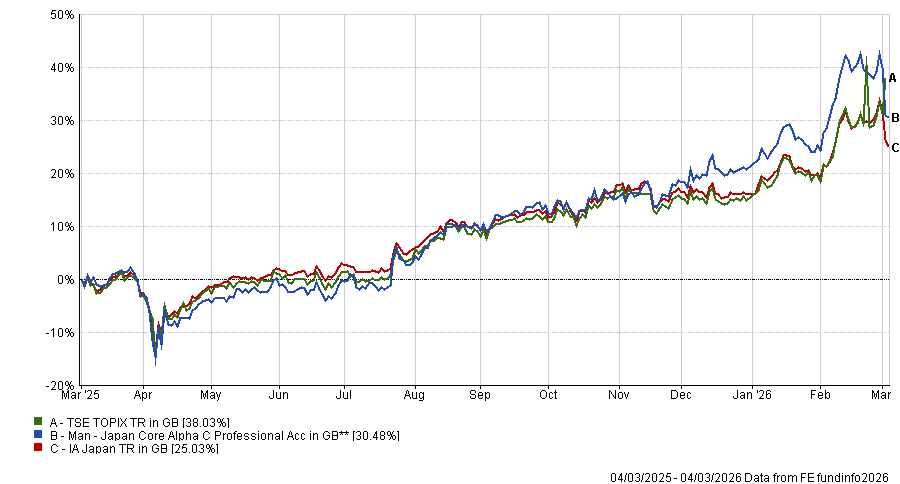

Performance of fund against index and sector over 1yr

Source: FE Analytics

Please describe the philosophy and process behind Man Japan Core Alpha

We take a contrarian value approach to Japanese large-caps, investing in depressed and unfashionable assets – stocks that are selling at a discount to their long-term average. We try to exploit extremes of valuation. One phrase we like to use is that we buy the stocks investors want to buy – they just don’t know it yet.

Valuation is critical. We look at it in absolute terms but also relative to the history of the stock. That approach typically aids us in avoiding investments in speculative bubbles and areas where valuations are aggressive. Historically it has worked very well in Japan because of the way mean reversion operates here.

Japan has long had a reputation for being cheap for structural rather than cyclical reasons. How do you avoid value traps?

I think Japan has had that reputation but we are seeing more change now than in the previous 30 years, and it’s been driven by the corporate governance revolution. The value that has long been locked up inside Japanese companies is finally being unveiled.

We’re less interested in the more simplistic approach of looking at companies with excess cash or excess cross-shareholdings. What we’re looking at is companies with radical management teams that want to conduct big structural change – focusing on return on capital, cost of capital, spinning off low-margin businesses and thinking in a more global way.

When we’re investing in unfashionable assets, we want to know that eventually there will be a reason or a catalyst for other investors to want to buy that stock. The headwinds facing the valuation and share price at that point should be because of excessive negativity, rather than justified negativity. Greed and fear are always present in markets and that’s what we’re trying to exploit.

Why should investors pick this fund to access Japan?

Value has had a good run in Japan over the past five years and has outperformed growth. But if you look at valuation levels, the areas of froth and exuberance still lie within the growth sector, particularly AI-related names.

The price-to-sales of MSCI Japan growth is actually at a similar level to the dot-com boom. The valuation gap between growth and value remains historically wide.

Within value, we remain optimistic on the parts of the market that should benefit from the domestic reflation story – financials and asset-heavy domestic stocks. But we’re also looking at areas that are resolutely contrarian right now, including some low-beta domestic defensives and some of the AI-disrupted names.

The Japanese market, like others, has been very narrow. It’s close to an all-time high, but that has been led by a quite small selection of stocks. We’re finding ample opportunity outside of that.

What was your best call over the past 12 months?

Real estate, particularly developers. The sector was one of the best performers in Japan last year and was a key exposure for the strategy going into 2025. We’d held a top-10 position in Mitsubishi Estate, one of Japan’s largest developers, when it was trading at a 50% discount to net asset value. In our view, Mitsubishi Estate owns some of the highest-quality land and property in the whole of Asia.

At the time, asset-heavy businesses were deeply unfashionable – the market wanted asset-light. The stock sat at a discount despite record-high profits and vacancy rates in its dominant Marunouchi district of Tokyo declining to around 1%, with rents steadily rising.

What we saw last year was a significant shift in focus, from a dislike of asset-heavy businesses to a preference for them, particularly in Japan’s reflationary environment.

Between January 2025 and today, Mitsubishi Estate’s share price has increased by 130%, outperforming the wider market substantially. We first started building the position back in 2015.

And the worst?

The auto sector was one of the most challenging areas of the Japanese market last year and it was a key overweight for us. At a sector level, you had competition from China, uncertainty around electrification, a stronger yen and then tariffs – all of which weighed on valuations. The overall auto sector underperformed the TOPIX by 15%. Nissan and Honda underperformed by almost 40% and 30%, respectively.

This was an area largely untouched by the corporate governance revolution and catalysts at a global sector level remain uncertain. One lesson for us was the importance of focusing on stock-specific stories rather than relying on a broader turn in sentiment towards the sector.

Take Honda: if you look at the value of its motorcycle business plus the net cash position, that actually exceeds Honda’s current market cap – meaning the market is placing effectively zero value on the auto business.

We think there’s an interesting sum-of-the-parts angle there, particularly if management moves to unlock it. And Nissan is undergoing significant restructuring with a new management team that we think, so far, appears to be doing the right things.

What do you do outside of fund management?

I’m a big fan of yoga – Iyengar yoga in particular. It’s a way to completely switch off for an hour or so.

Important legal information

Lloyds and Lloyds Bank are trading names of Halifax Share Dealing Limited. The Lloyds Bank Direct Investments Service is operated by Halifax Share Dealing Limited. Registered Office: Trinity Road, Halifax, West Yorkshire, HX1 2RG. Registered in England and Wales no. 3195646. Halifax Share Dealing Limited is authorised and regulated by the Financial Conduct Authority, 12 Endeavour Square, London, E20 1JN under registration number 183332. A Member of the London Stock Exchange and an HM Revenue & Customs Approved ISA Manager.

The information contained within this website is provided by Allfunds Digital, S.L.U. acting through its business division Digital Look Ltd unless otherwise stated. The information is not intended to be advice or a recommendation to buy, sell or hold any of the shares, companies or investment vehicles mentioned, nor is it information meant to be a research recommendation. This is a solution powered by Allfunds Digital, S.L.U. acting through its business division Digital Look Ltd incorporating their prices, data news, charts, fundamentals and investor tools on this site. Terms and conditions apply. Prices and trades are provided by Allfunds Digital, S.L.U. acting through its business division Digital Look Ltd and are delayed by at least 15 minutes.

Data provided by FE fundinfo. Care has been taken to ensure that the information is correct, but FE fundinfo neither warrants, represents nor guarantees the contents of information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Past performance does not predict future performance, it should not be the main or sole reason for making an investment decision. The value of investments and any income from them can fall as well as rise.

© 2026 Refinitiv, an LSEG business. All rights reserved.